At the Edge of Chaos: Elvis Has Left the Building. Selling is About to Pick Up Some Speed.

It looks as if the proverbial “Elvis has left the building” moment has finally arrived on Wall Street.

That’s because the rapidly withering market breadth is a sign that buyers are mostly gone, while the sudden resurgence of short-sellers suggests that the selling spree is about to pick up speed. So either we’re about to get a really big bounce because there are no bulls left, or the selling is about to accelerate.

Why the Bears Are Right for Now

A recent Rasmussen poll reported that 57% of Americans think that a 1930s-like Depression is possible within the next few years. That’s a 2% increase from a similar poll conducted by Rasmussen in May 2022. A more recent poll reported that 64% of Americans think we are currently in a recession.

If that’s not a sign that we are living through a major wall of worry in the real world, then I don’t know what is.

So, with so much fear in the air, why aren’t stocks bouncing convincingly? Spoiler alert: liquidity.

Why the Fed is Wrong

My thoughts on the Federal Reserve and its current anti-inflation crusade are well-known, but worth summarizing in one phrase. This inflationary cycle is a structural supply side squeeze, not the traditional “too many dollars chasing too few goods” scenario. Consider the following:

The Fed, even if they went too far, correctly responded to COVID shutdowns by its QE maneuvers. Unfortunately for the Fed, the current inflation was set up by factors only partially related to monetary policy, which was by no means perfect over the last several decades.This bout of inflation is more due to the lack of regional manufacturing capacity resulting from the effects of globalization than to the Fed’s massive QE in response to COVID.Because there isn’t enough manufacturing capacity to meet demand for products, in the face of large amounts of money from QE, prices are going up.This bout of inflation isn’t exclusively a monetary problem, it’s also a fiscal policy problem and a corporate problem due to indiscriminate government spending, in addition to being the result of companies who moved their manufacturing capacity overseas to increase profits, reducing the U.S. manufacturing sector dramatically.Thus, even when the effect of Congress’s unending spending spree is ignored, until regional manufacturing capacity is restored or improved, inflation isn’t going to respond meaningfully to the Fed’s rate hikes – until the economy falls apart.

The net effect is that the interest rate increases have done little to reduce inflation because demand remains stable or rising, while not enough new factories to produce the goods being demanded – food, gasoline, and housing – are domestically available to fill the market’s needs. So, while there aren’t enough things being made due to structural problems that the Fed had nothing to do with, what the central bank is currently doing will never work until the structural supply side of the economy is repaired.

Thus, what the central bank has accomplished is to radically reduce the global dollar supply. This, in turn, is creating a situation where, at some point, there won’t be enough money in circulation to finance the purchase of what’s available even at inflationary prices.

In plain language, this is creating an economic stall.

Moreover, because the financial markets are the main drivers of the economy, by choking the financial markets, the Fed is now threatening the real economy both by reducing the money supply and by severely affecting a critical income stream for businesses and individuals.

Mission accomplished.

Is the Capitulation Phase Here?

Stocks rallied on 9/28 as the Bank of England (BOE) announced a bond buy back and currency intervention program to calm its bond market and to attempt to stabilize the Pound Sterling. This was widely heralded as the restart of QE. Other central banks, South Korea and Taiwan, announced similar actions.

But it didn’t last.

In fact, as I describe below, the market’s technicals suggest that a new wave of asset selling is about to pick up steam, as the market and the economy have melded into one single system. Plainly stated, when stocks tank, the economy follows.

What the BOE has learned the hard way is that central banks have created a new economic dynamic in which the machine traders make huge and fast bets on every word uttered by a central banker. In addition, because of the high level of debt in the world, both corporate and personal, most people can’t make ends meet based on their job(s), while businesses depend on cash flow to stay open.

The answer to both problems is the stock market, and the subsequent wealth effect created by higher stock prices. Whether central bankers or traditional economists like it, stock prices are now the central factor influencing spending habits. Moreover, without sustained high liquidity from central banks, the system no longer functions.

So yes, as I’ve been saying here for quite a while, the financial markets and the economy are now one system, the MELA (Markets, Economy, Life Decisions, and Algos). And when the markets reach certain points of stress, the whole thing tends to crash as the algos make everything happen faster.

There is no room for error. Yet, it seems they are making a really big one here.

Welcome to the Edge of Chaos:

“The edge of chaos is a transition space between order and disorder that is hypothesized to exist within a wide variety of systems. This transition zone is a region of bounded instability that engenders a constant dynamic interplay between order and disorder.” – Complexity Labs

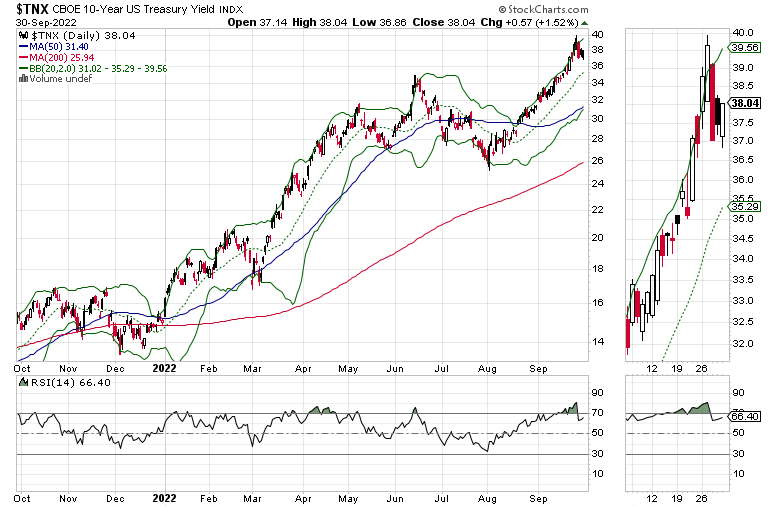

Bonds Are Extremely Oversold

The bond market is caught between rocketing yields higher due to inflation or starting to factor in that the economy is near a point of stalling. Moreover, given the level where the RSI indicator currently resides for most yields (well above 70, meaning the yields are well over-extended), it is plausible that, when there are enough signs of economic weakness, the reversal in yields will likely be very impressive.

The U.S. Ten Year note yield (TNX) tested the 4% yield and failed, but remained above 3.75%. That means that we may be in a trading range for a while.

The U.S. Two-Year Note yield (UST2Y) remains well above 4%.

Interestingly, the Eurodollar Index (XED) may be flattening out. If this were to continue, it would mean that liquidity is starting to stabilize.

Check out my recent Your Daily Five video on how to adjust your trading based on liquidity.

Terrible Breadth, and Falling ADI and OBV are Ominous Signs for Stocks

Because there is no liquidity, short sellers are coming back, just as the buyers are leaving the market faster.

Note the rolling over of the Accumulation Distribution line (ADI), coupled with the continued decline in On Balance Volume (OBV) for the S&P 500 (SPX).

Falling ADI means short-sellers are back, while the decline in OBV means that the buyers are accelerating their run for the exits.

And since price is the ultimate truth, note that SPX continues to slice through support levels ,as the very important 3900 area gave way easily and the selling mounted.

The New York Stock Exchange Advance Decline line (NYAD) remains oversold, with its RSI near 30 and the line moving back inside the lower Bollinger Band (green lower line). If NYAD starts to slide lower while remaining inside the lower band, it will be a sign that the selling will continue for a while, at least until it falls outside the band again.

VIX may have topped out, which may or may not be bullish depending on the actual price action. Meanwhile, XED is flat, but nowhere near bullish, which means that, even though fear and technical developments are ripe for a rally, money to fuel the rally is still scarce.

The Nasdaq 100 index (NDX) mirrors the action in SPX, although the price activity is likely to be a bit worse. NDX did no better as it got crushed further after failing to bounce back to 13,000.

To get the latest up-to-date information on options trading, check out Options Trading for Dummies, now in its 4th Edition – Get Your Copy Now! Now also available in Audible audiobook format!

#1 New Release on Options Trading!

Good news! I’ve made my NYAD-Complexity – Chaos chart (featured on my YD5 videos) and a few other favorites public. You can find them here.

Joe Duarte

In The Money Options

Joe Duarte is a former money manager, an active trader and a widely recognized independent stock market analyst since 1987. He is author of eight investment books, including the best selling Trading Options for Dummies, rated a TOP Options Book for 2018 by Benzinga.com and now in its third edition, plus The Everything Investing in Your 20s and 30s Book and six other trading books.

The Everything Investing in Your 20s and 30s Book is available at Amazon and Barnes and Noble. It has also been recommended as a Washington Post Color of Money Book of the Month.

To receive Joe’s exclusive stock, option and ETF recommendations, in your mailbox every week visit https://joeduarteinthemoneyoptions.com/secure/order_email.asp.